By Otto Acosta, Offerpad Research Team

For most of 2024, the conventional wisdom in real estate was simple. Commissions were about to fall, maybe by a lot. A landmark legal settlement was rewriting the rules on how agents get paid, and buyers and sellers braced for a discount.

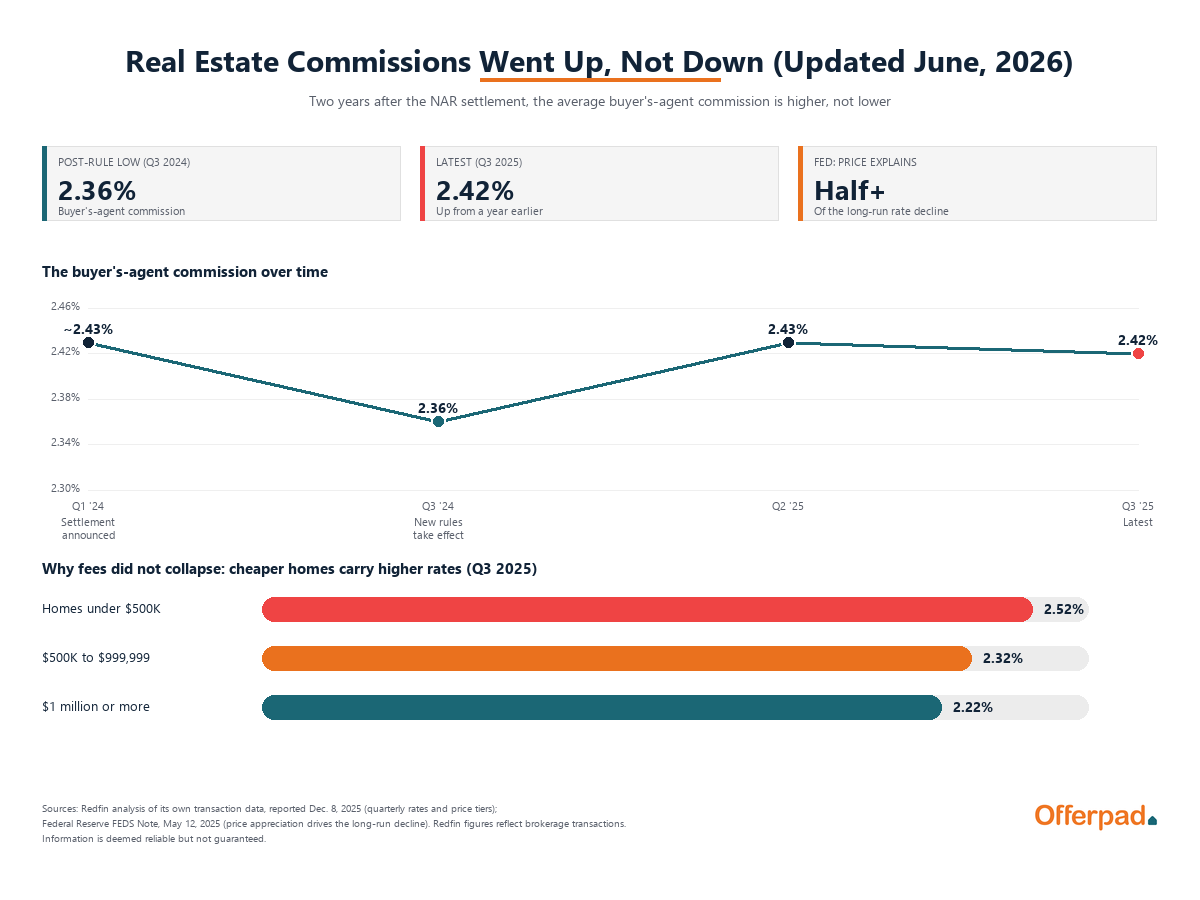

Nearly two years on, the discount has not arrived. The fee a buyer’s agent earns is slightly higher today than it was when the new rules began. The full cost of selling a home, both agents combined, still sits in the same mid-5 percent range it occupied before anyone went to court.

The reason is not that the rules failed. A different force has been setting commission rates all along, and it has little to do with lawsuits. It is the price of homes.

Did the Settlement Lower Real Estate Commissions?

Not so far. A Federal Reserve analysis published May 12, 2025 looked at nearly three decades of real estate commissions and found that the rate a buyer’s agent charges has been drifting down slowly for a long time, from about 3 percent in the late 1990s to about 2.7 percent today (Federal Reserve).

What pushed it down was not regulation. It was appreciation. The Fed economists calculated that the doubling of home prices since the mid-1990s cut commission rates by about 0.2 percentage point, which is more than half of the entire nationwide decline over that period. The logic is plain once you see it. A 3 percent fee on a $150,000 home is $4,500. As that same home climbs toward $400,000, the same percentage produces a much larger check, and the rate tends to ease. When prices climb, the percentage drifts down on its own. When the market slows, that pressure fades.

The Fed also tested the kinds of rules the settlement put in place. It examined written buyer-representation agreements and bans on agent rebates in states that had adopted them before the national changes, and found “very small negative effects of just a few basis points, neither of which is statistically distinguishable from zero.” Similar rules, where they had been tried, moved commissions by close to nothing.

What the Settlement Actually Changed

The settlement was real, and large. The National Association of Realtors (NAR) agreed to pay $418 million and to change how the business works, after a jury found it had conspired with large brokerages to keep agent commissions high. The new rules took effect August 17, 2024 (NAR).

Two changes drew the most attention. First, offers of compensation can no longer appear inside a multiple listing service (MLS), the regional databases agents use to share listings. For decades, a seller’s agent would advertise, within the MLS, how much a buyer’s agent would be paid for bringing a buyer. That line is now gone. Second, agents working with buyers must sign a written agreement with those buyers before touring a home. The agreement has to state the fee as a specific amount or rate, cap the agent’s compensation at that figure, and include a plain statement that broker fees “are fully negotiable and not set by law.”

The theory was that buyers, now seeing a fee in writing and signing for it directly, would negotiate harder, and that pulling the advertised payment out of the MLS would loosen an informal standard that had parked most commissions near a familiar number. NAR’s own summary stresses that compensation “continues to be fully negotiable.”

Where Did Commissions Actually Go?

Up. Redfin, a national brokerage, tracks the buyer’s-agent commission every quarter from the deals it handles. The rate fell to a low of 2.36 percent in the third quarter of 2024, the quarter the new rules began. Then it climbed back.

| Period | Average Buyer’s-Agent Commission |

|---|---|

| Q1 2024 (settlement announced) | about 2.43% |

| Q3 2024 (new rules take effect) | 2.36% |

| Q2 2025 | 2.43% |

| Q3 2025 | 2.42% |

Source: Redfin analysis of its own transaction data, reported Dec. 8, 2025 (redfin.com). Redfin is a real estate brokerage; the figures reflect transactions it handled.

In the third quarter of 2025, the average buyer’s-agent commission was 2.42 percent, up from 2.36 percent a year earlier (Redfin). That put the rate back near where it sat in early 2024, before the rules took effect. A separate Redfin reading, reported by CNBC in August 2025, showed the spring 2025 figure at 2.43 percent, up from 2.38 percent a year before (CNBC). The two readings cover different quarters, and both move in the same direction.

The explanation, according to those same reports, is the state of the housing market rather than the rules. Home sales were slow through 2025 and the number of unsold homes kept climbing, which handed buyers the upper hand. Buyers used that leverage in an unexpected way. Instead of negotiating their own agent’s fee down, they pressed sellers to keep paying it. As the reporting on Redfin’s data put it, buyer agents “are still getting paid by the home seller and commission rates have actually increased” (Real Estate News). In a buyer’s market, a buyer can walk to the next listing if a seller balks. Most sellers paid.

Why Are Commission Rates Higher on Cheaper Homes?

The single clearest illustration of why prices drive commissions sits inside Redfin’s own breakdown by home value. The cheaper the home, the higher the percentage the buyer’s agent earns.

| Home Price | Buyer’s-Agent Commission (Q3 2025) | A Year Earlier |

|---|---|---|

| Under $500,000 | 2.52% | 2.45% |

| $500,000 to $999,999 | 2.32% | 2.31% |

| $1 million or more | 2.22% | 2.24% |

Source: Redfin analysis of its own transaction data, reported Dec. 8, 2025 (redfin.com).

A home under $500,000 carried a 2.52 percent buyer’s-agent fee. A home over $1 million carried 2.22 percent. On a $300,000 home, 2.52 percent is about $7,560. On a $1.2 million home, 2.22 percent is about $26,640. The dollar payout still rises sharply with price, so a lower percentage on an expensive home can still mean a far larger check. That is the appreciation effect the Federal Reserve identified, captured in a single quarter rather than across thirty years.

It is also where the recent increase concentrated. The rate rose in the two lower price bands and slipped only in the million-dollar-plus band, which suggests the upward pressure came from the broad middle of the market, where most homes trade.

What Is the Average Real Estate Commission in 2026?

The buyer’s-agent commission is only one side of the bill. A seller traditionally pays both the listing agent and the buyer’s agent. Add them together and the total is the number most sellers care about. Two industry surveys put it in the mid-5 percent range, well within the historical norm and far from the collapse some predicted.

A February 2026 survey of 533 partner agents by Clever Real Estate, a referral company, put the average total commission at about 5.70 percent, split into a 2.88 percent listing-side fee and a 2.82 percent buyer’s-side fee (Clever). A separate survey of 580 agents by the referral firm FastExpert, fielded in early 2025, put the national average total commission at 5.57 percent (FastExpert). Both are survey estimates rather than transaction records, and they differ by methodology and sample. Both land in the same range. A typical home sale still carries combined agent fees of roughly 5.5 to 5.7 percent, the way it largely has for years.

What Is the Real Estate Commission Rate in Your State?

National averages hide a wide spread. The Clever survey reported combined commission rates for every state, ranging from 4.50 percent in Washington, D.C., to 6.20 percent in Michigan (Clever). The full survey table is below. These are survey estimates, and the fee on any single sale is negotiable.

| State | Total | State | Total |

|---|---|---|---|

| Alabama | 5.96% | Montana | 5.71% |

| Alaska | 5.51% | Nebraska | 5.84% |

| Arizona | 5.82% | Nevada | 5.71% |

| Arkansas | 5.66% | New Hampshire | 5.57% |

| California | 5.47% | New Jersey | 5.20% |

| Colorado | 5.71% | New Mexico | 5.82% |

| Connecticut | 5.57% | New York | 5.69% |

| Delaware | 5.66% | North Carolina | 5.53% |

| Florida | 5.57% | North Dakota | 5.84% |

| Georgia | 5.66% | Ohio | 5.90% |

| Hawaii | 5.51% | Oklahoma | 5.82% |

| Idaho | 5.71% | Oregon | 5.51% |

| Illinois | 5.53% | Pennsylvania | 5.77% |

| Indiana | 5.50% | Rhode Island | 5.57% |

| Iowa | 5.84% | South Carolina | 5.88% |

| Kansas | 5.84% | South Dakota | 5.84% |

| Kentucky | 5.66% | Tennessee | 6.05% |

| Louisiana | 5.66% | Texas | 5.88% |

| Maine | 5.57% | Utah | 5.71% |

| Maryland | 5.41% | Vermont | 5.57% |

| Massachusetts | 5.57% | Virginia | 5.50% |

| Michigan | 6.20% | Washington | 5.90% |

| Minnesota | 5.84% | Washington, D.C. | 4.50% |

| Mississippi | 5.66% | West Virginia | 5.66% |

| Missouri | 5.94% | Wisconsin | 5.84% |

| Wyoming | 5.71% |

Source: Clever Real Estate survey of 533 partner agents, February 2026 (listwithclever.com). Survey estimates, not transaction data.

The spread tracks home prices, the same way the buyer’s-agent rate does. Some of the highest rates show up in more affordable states, including Michigan (6.20 percent), Tennessee (6.05 percent), and Missouri (5.94 percent). Some of the lowest show up in higher-cost places, including Washington, D.C. (4.50 percent) and California (5.47 percent). The Federal Reserve found the same regional pattern. Rates run lower in the Northeast, in California, and in the Pacific Northwest, the areas with the most expensive housing, and the typical New York metropolitan rate sits at 2 percent per side (Federal Reserve). Wherever homes cost more, the percentage tends to be smaller. The table offers a rough local benchmark, with the understanding that the actual fee on any one sale is negotiated deal by deal.

What Changed for Buyers and Sellers in Practice

If the price did not move much, something did. The change was in how the fee shows up, not how large it is.

- Buyers now sign a written agreement with their agent, with the fee named, before touring a home. The cost is visible earlier in the process than it used to be.

- Sellers no longer see a buyer’s-agent commission advertised inside the MLS, and are no longer automatically expected to set one there.

- Compensation to a buyer’s agent is now a separate negotiation. Sellers can still offer it, and in the current buyer-friendly market, most do.

NAR’s summary stresses that “agent compensation for home buyers and sellers continues to be fully negotiable” (NAR). The clearest practical change is transparency, not price. The fee is disclosed sooner and labeled as negotiable. More buyers and sellers are seeing the number than were before, while the number itself has held roughly steady, with a recent tilt upward. Agents have adapted as well, with some leaning on referral and partnership programs that pay a fee without a traditional listing.

Will Commissions Fall Later?

There is a catch worth stating plainly. The recent increase rode on a slow market that favored buyers. When demand returns and sellers regain leverage, they may be less willing to keep covering the buyer’s-agent fee. The trade press has flagged exactly this: “it remains to be seen whether sellers will still pay once demand picks up and they gain more leverage” (Real Estate News).

For now, the verdict on the commission shakeup is the opposite of what almost everyone predicted. Two years after the rules changed, the fees went up.

Methodology

This article draws on public and third-party sources. The long-run trend and the explanation for it come from the Federal Reserve FEDS Note “Commissions and Omissions: Trends in Real Estate Broker Compensation,” published May 12, 2025, which analyzed CoreLogic multiple listing service data from 1995 through 2023 (federalreserve.gov).

Quarterly buyer’s-agent commission rates are from Redfin, a real estate brokerage, based on its own transaction records and reported December 8, 2025 (redfin.com), with corroborating spring 2025 figures reported by CNBC on August 26, 2025 (cnbc.com) and Real Estate News on August 16, 2025 (realestatenews.com).

Total commission rates and the state-by-state figures are survey estimates: a February 2026 survey of 533 partner agents by Clever Real Estate (listwithclever.com) and an early-2025 survey of 580 agents by FastExpert (fastexpert.com). Survey-based estimates differ from transaction records and from one another by methodology and sample.

Settlement details are from the National Association of Realtors (nar.realtor). Commission rates are negotiable and vary by agent, market, price, and property. Information is deemed reliable but not guaranteed.