By Otto Acosta, Offerpad Research Team

Every spring, the same question surfaces in real estate conversations across the country: When is the best time to sell a house?

The answer moves real money. Across 15 major U.S. metros where Offerpad operates, homes sell for about 4.2% above the year’s average price in June, the annual high, and about 7.0% below it in January, the annual low. That is a swing of roughly 11 percentage points on the same kind of home in the same city, separated only by the calendar.

To see where that timing matters most, and where it barely matters at all, we looked at public market data from the Redfin Data Center, covering single-family home sales across the 15 metros where Offerpad buys and sells homes. The seasonal patterns below come from that data, not from any one company’s transactions.

Best Month to Sell a House: Price, Speed, and Competition

The best time to sell a house depends on what you care about most. The table below shows the strongest and weakest month for each selling metric, averaged across the 15 metros in the analysis.

| Seller Priority | Best Month | 15-Metro Average | Worst Month | 15-Metro Average |

|---|---|---|---|---|

| Highest sale price (vs. yearly average) | June | +4.2% | January | -7.0% |

| Fastest sale (days on market) | May | 30.0 days | December | 50.3 days |

| Most above-list sales | May | 37.9% | December | 21.8% |

| Strongest sale-to-list ratio | May | 100.3% | December | 98.2% |

The peaks do not all land in the same month, and that is down to the lag between listing and closing. Homes listed in April and May get showings, draw offers, and enter escrow over the following weeks. That spring listing rush shows up as a June price peak, when the strongest offers finally close. Competition and speed, on the other hand, top out a little earlier, in May, when buyer demand is highest relative to the homes on the market.

The worst stretch to sell is the middle of winter. Prices bottom out in January, sitting about 7.0% below the year’s average, with February close behind at 5.2% below. Homes also move slowest and draw the fewest competing offers heading into the holidays: December sees the longest time on market (about 50 days) and the smallest share of homes selling above list (21.8%). Sellers who list in winter often have a reason that overrides timing, such as a job relocation, a family change, or a financial deadline.

When to Sell a House: Month-by-Month Breakdown

The table below shows how each selling metric shifts across the calendar year, averaged across the 15 metros and all available years.

| Month | Days on Market | Price vs. Yearly Avg. | % Sold Above List | Sale-to-List Ratio |

|---|---|---|---|---|

| January | 48.0 | -7.0% | 24.2% | 98.4% |

| February | 47.6 | -5.2% | 27.2% | 98.9% |

| March | 38.9 | -2.3% | 31.8% | 99.5% |

| April | 31.9 | +0.2% | 36.2% | 100.1% |

| May | 30.0 | +2.5% | 37.9% | 100.3% |

| June | 30.5 | +4.2% | 37.2% | 100.1% |

| July | 32.3 | +3.3% | 34.4% | 99.7% |

| August | 36.0 | +2.0% | 29.8% | 99.1% |

| September | 40.2 | +0.8% | 26.5% | 98.8% |

| October | 42.3 | +0.7% | 25.1% | 98.6% |

| November | 44.7 | +0.4% | 23.6% | 98.4% |

| December | 50.3 | +0.4% | 21.8% | 98.2% |

Source: Redfin Data Center, single-family homes, 15 metro areas, monthly 2021-2025. Price vs. yearly average is each month’s median relative to the year’s average. See methodology.

January and February are the trough. Homes sit longest, sell for the least, and face the weakest buyer competition. From February to April the market wakes up fast: days on market falls from about 48 to 32, and the share of homes selling above list climbs from 27.2% to 36.2%. Buyers who spent the winter browsing start writing offers once more homes come to market.

The best time to sell a house is the April-through-July window. Those four months carry the fastest sales, the highest prices, the most bidding wars, and the strongest sale-to-list ratios. Within that stretch, May and June are the twin peaks. May has the most competitive market, with 37.9% of homes selling above list and the fastest sales of the year at 30.0 days, while June brings the highest prices, running 4.2% above the yearly average.

Then the fade sets in. By September, days on market has crept back up toward 40 and the share of above-list sales has dropped to 26.5%. Families settle into the school year and buyer urgency cools. October and November hold up better on price than the raw calendar might suggest, but competition keeps thinning into the holidays.

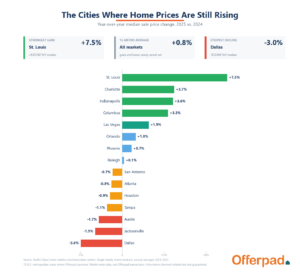

Best Time to Sell a House by City: Where Seasonality Hits Hardest

National averages hide wide differences between cities. One clean way to measure how much timing matters in a given market is the spread between its best and worst month for price, expressed as points above or below that market’s own yearly average. The table below ranks all 15 metros by that spread.

| Rank | Market | Best-to-Worst Spread | Peak Month | Trough Month |

|---|---|---|---|---|

| 1 | St. Louis | 20.2 pts | June (+9.4%) | January (-10.8%) |

| 2 | Columbus | 17.0 pts | June (+5.9%) | January (-11.1%) |

| 3 | Indianapolis | 12.9 pts | July (+4.4%) | January (-8.5%) |

| 4 | Atlanta | 12.9 pts | June (+5.4%) | January (-7.5%) |

| 5 | Dallas | 12.4 pts | June (+4.9%) | January (-7.5%) |

| 6 | Austin | 12.2 pts | June (+5.1%) | January (-7.1%) |

| 7 | Raleigh | 11.6 pts | July (+4.1%) | February (-7.5%) |

| 8 | Charlotte | 10.9 pts | June (+4.9%) | January (-6.1%) |

| 9 | Houston | 10.5 pts | June (+4.0%) | January (-6.5%) |

| 10 | Jacksonville | 9.4 pts | June (+3.1%) | January (-6.3%) |

| 11 | Tampa | 9.2 pts | June (+2.9%) | January (-6.3%) |

| 12 | Orlando | 8.4 pts | November (+2.4%) | January (-6.0%) |

| 13 | San Antonio | 8.2 pts | June (+2.9%) | January (-5.3%) |

| 14 | Las Vegas | 7.4 pts | July (+2.4%) | January (-5.1%) |

| 15 | Phoenix | 6.4 pts | May (+2.1%) | January (-4.3%) |

Source: Redfin Data Center, single-family homes, monthly 2021-2025. Spread is the gap in points between each market’s best and worst month, measured against its own yearly average.

Two patterns stand out. Markets with cold winters and a sharp spring thaw show the biggest swings, while warm-weather Sun Belt cities stay steadier year-round.

High-swing markets: St. Louis, Columbus, Indianapolis, and Atlanta. These four see the largest gaps between their best and worst months, from about 13 points in Atlanta and Indianapolis to more than 20 in St. Louis. Most sit in the Midwest and Southeast, where a slow winter gives way to a crowded spring. Sellers here gain the most by lining up a spring listing for a late-spring or summer close.

Austin is worth a second look. It does not get cold enough to freeze buyers out, yet it shows one of the wider swings in the group at 12.2 points. The reason is likely its economy rather than its weather. Austin’s tech sector runs on corporate hiring cycles that pack relocations into spring and early summer, so demand surges when the big employers bring in new hires and cools when they pause.

Low-swing markets: Phoenix, Las Vegas, San Antonio, and Orlando. These cities show the smallest seasonal price gaps, from 6.4 points in Phoenix to 8.4 in Orlando. Year-round migration, retiree moves, and steady warm weather keep demand more even across the calendar. Orlando is a small exception to the summer-peak rule: its strongest month for price is November, when winter buyers from the North start shopping.

Home Sale Prices by Season: What Timing Is Worth

Zoom out from individual months and the seasonal shape gets clearer. The table below averages each month’s price position into four seasons, across all 15 metros.

| Season | Price vs. Yearly Avg. |

|---|---|

| Summer (Jun-Aug) | +3.1% |

| Fall (Sep-Nov) | +0.6% |

| Spring (Mar-May) | +0.1% |

| Winter (Dec-Feb) | -3.9% |

Summer closings are the strongest, running about 3.1% above the yearly average, because they capture the offers written during the busy spring. Winter closings are the weakest at about 3.9% below average. Spring itself lands near neutral once you average its months together, since the sharp climb from March into May starts from a soft winter base.

How much that costs depends heavily on the market. Take St. Louis, the widest-swinging metro in the group. Its price runs about 9.4% above the yearly average in June and about 10.8% below in January, a 20.2-point spread. Applied to St. Louis’s 2025 median sale price of roughly $288,554, that gap works out to about $58,000 as an illustrative example. Same house, same neighborhood, same school district, with the month as the only variable. At the other end, Phoenix barely moves. Its 6.4-point spread is the smallest of any metro, so a Phoenix seller faces almost no price penalty for selling at the “wrong” time. For those sellers, the best time to sell is whenever the home is ready.

Bidding Wars by Month: When Homes Sell Above Asking Price

The share of homes selling above list price is one of the clearest reads on buyer competition. Across the 15 metros, that share peaks at 37.9% in May and bottoms out at 21.8% in December. As with price, the market-level picture is where it gets interesting.

| Market | Trough | Peak | Seasonal Swing |

|---|---|---|---|

| Columbus | Dec: 29.7% | May: 53.8% | 24.1 pp |

| St. Louis | Jan: 33.3% | Jun: 55.3% | 22.0 pp |

| Austin | Dec: 17.8% | Apr: 38.9% | 21.1 pp |

| Dallas | Dec: 21.1% | May: 41.8% | 20.7 pp |

| Raleigh | Dec: 24.9% | May: 44.6% | 19.7 pp |

| Indianapolis | Dec: 19.8% | May: 38.7% | 18.9 pp |

| Charlotte | Dec: 24.7% | May: 41.5% | 16.8 pp |

| Atlanta | Dec: 24.7% | May: 41.3% | 16.6 pp |

| Las Vegas | Dec: 21.5% | May: 37.1% | 15.6 pp |

| Phoenix | Dec: 19.5% | May: 33.8% | 14.3 pp |

| Houston | Dec: 15.9% | Jun: 29.0% | 13.1 pp |

| San Antonio | Nov: 19.0% | Jun: 30.5% | 11.5 pp |

| Tampa | Dec: 18.7% | May: 30.1% | 11.4 pp |

| Orlando | Dec: 17.1% | Jun: 28.2% | 11.1 pp |

| Jacksonville | Dec: 17.0% | May: 26.9% | 9.9 pp |

Source: Redfin Data Center, single-family homes, monthly 2021-2025. Swing is the gap in percentage points (pp) between each market’s peak and trough month.

Columbus and St. Louis lead the bidding-war tables. In Columbus, more than half of May sales close above asking (53.8%). In St. Louis, that figure tops 55% in June, so more homes sell above list than below it. Both are affordable Midwestern markets where strong spring demand meets thin inventory, and the result is fierce competition. At the other end, Jacksonville and Orlando show the smallest swings, holding roughly between 17% and 28% across their calendars.

Markets with the widest price swings tend to have the widest bidding-war swings too, which points to the same seasonal forces driving both prices and competition.

What This Means for Sellers in 2026

The data gives sellers a framework for reading the seasonal forces in their own market.

In high-swing markets, timing carries real weight. In St. Louis and Columbus, the gap between the best and worst month runs 17 to 20 points of a home’s typical price. Lining up an April or May listing for a June or July close stacks the odds toward higher prices, faster sales, and more competitive offers.

In low-swing markets, other factors matter more. Phoenix, Orlando, San Antonio, and Las Vegas show the smallest seasonal price gaps. For sellers there, home condition, accurate pricing, and local neighborhood dynamics will usually decide the outcome more than the month on the calendar.

Speed and price do not peak in the same month. The fastest sales come in May (30.0 days) and the highest prices in June (+4.2%). Sellers who care most about a quick sale may do best listing a little earlier in the spring.

January and February are the toughest months to sell by nearly every measure. Prices, speed, and buyer competition all sit at their annual lows. Sellers who can avoid listing in the dead of winter will, on average, meet better conditions.

Of course, the calendar is only one input, and not every seller can wait for spring. If a move, a job, or a deadline lands in the off-season, it helps to compare your options side by side. Some sellers list with an agent; others weigh a no-obligation cash offer from Offerpad so they can pick a closing date that fits their timeline. You choose the path that works best for your situation.

Methodology

This analysis is based on market-wide data from the Redfin Data Center for single-family home sales, compiled by the Offerpad Research Team. It covers monthly data from 2021 through 2025 across the 15 metropolitan markets where Offerpad operates and where Redfin publishes metro-level data: Atlanta, Austin, Charlotte, Columbus (OH), Dallas, Houston, Indianapolis, Jacksonville, Las Vegas, Orlando, Phoenix, Raleigh, St. Louis, San Antonio, and Tampa. Columbia, SC is not covered by Redfin’s metro market tracker and is excluded from this analysis.

All figures represent market-wide transaction data, not Offerpad transactions. Seasonal averages are computed for each calendar month across the years in the dataset. “Price vs. yearly average” measures how a given month’s median sale price compares with the average for its year, expressed as a percentage above or below. Days on market measures the time from listing to contract. Percent sold above list is the share of transactions where the final sale price exceeded the list price. Sale-to-list ratio is the average of final sale price divided by list price. The best-to-worst spread and seasonal swings are calculated within each market against its own yearly average.

Data provided by the Redfin Data Center. Information deemed reliable but not guaranteed.